justice requires wealthy countries to compensate the poor for the damage that climate change causes them

has been weakened both by global rules that favour profit shifting and by domestic policies shaped by those who benefit most from the status quo

Climate finance is often framed as a search for new money. Our analysis and the climate finance slider released with this report, shows that the real issue is not scarcity but capture. Extreme wealth and undertaxed multinational profits are plentiful; what is missing is countries’ ability and willingness to tax them. This ability, tax sovereignty, […]

'Scarcity to address the climate crisis comes not from a genuine lack of resources but from elite capture and a lack of tax sovereignty on the part of countries' ~ Franziska Mager

'Scarcity to address the climate crisis comes not from a genuine lack of resources but from elite capture and a lack of tax sovereignty on the part of countries' ~ Franziska Mager #SB62 #ClimateFinance #BonnClimateConference

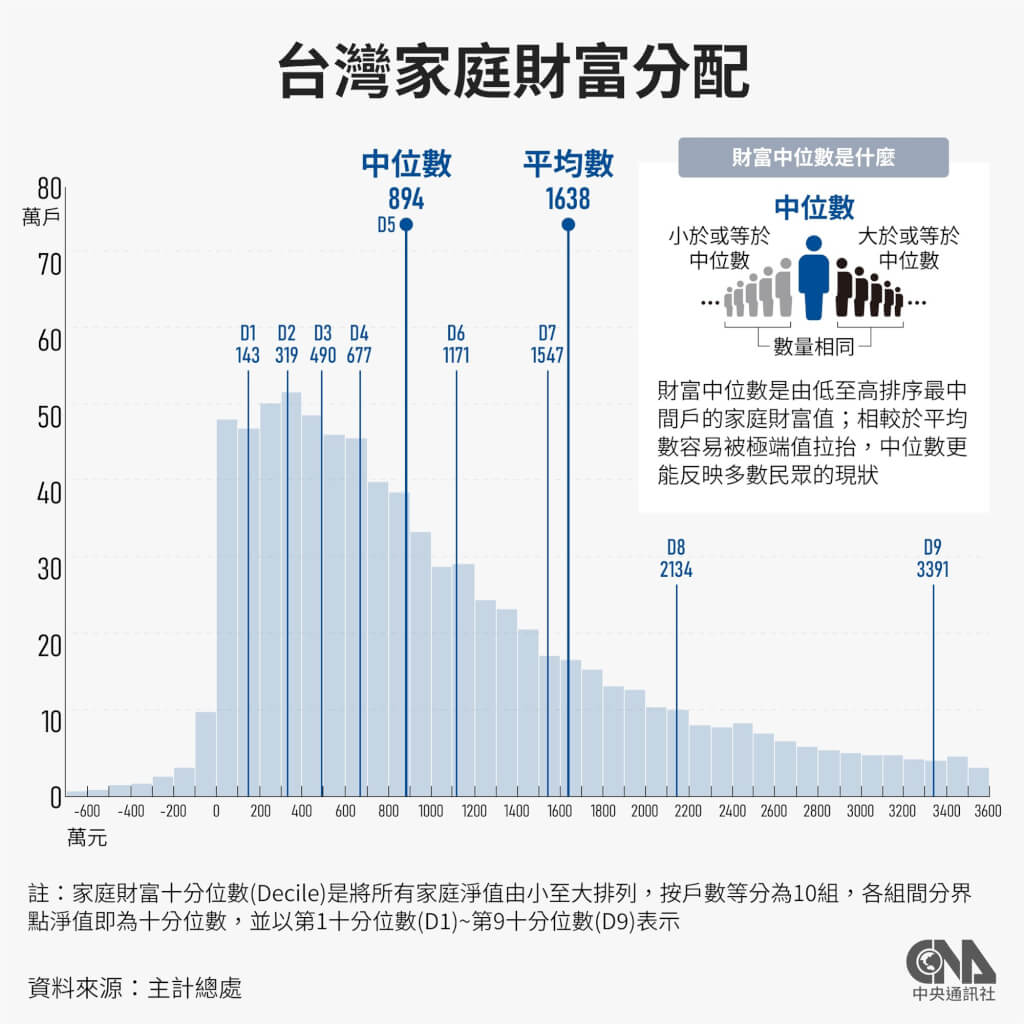

主計總處時隔30年再次發布國富統計報告,公布台灣家庭財富分配統計結果,民國110年最富裕的20%家庭財富是新台幣5133萬元,財富資產最少的20%家庭,平均每戶僅有77萬元;兩族群差距高達66.9倍,明顯比民國80年差距16.8倍大很多。

後20%家庭佔不到1%財富, 平均欠債卻最高達405萬元

早些年遺贈稅的確採用累進方式,最高稅率達50%,後來馬政府卻大幅調降至10%單一稅率,即使蔡政府將遺贈稅些微提高到20%(中間有分15%級距)

睽違30年,主計總處再次公布家庭財富分配統計,顯示貧富差距擴大,外界關注下一次公布統計是何時,主計總處主計長朱澤民表示,隨著調查技術與大數據發展,接下來會定期發布統計,「我認為4年做一次很恰當」。

the deliberate weakening of social protections has produced greater financial and economic insecurity

Joseph E. Stiglitz considers what 40 years of anti-government, low-tax, deregulatory advocacy have wrought around the world.

people suffering from precarity, which means existing without predictability or security, affecting material or psychological welfare ... lack of job security

In sociology and economics, the precariat (/prɪˈkɛəriət/) is a neologism for a social class formed by people suffering from precarity, which means existing without predictability or security, affecting material or psychological welfare. The term is a portmanteau merging precarious with proletariat.[1] Unlike the proletariat class of...

蒲公英族(英語:precariat;/prɪˈkɛəriət/),或譯作「流眾」[1]、「不穩定無產者」[2]、「殆危族」、「飄零族」[3][4]等,在社会学和经济学中,是由飽受不稳定之苦的人组成的階級。蒲公英族是不稳定(precarious)与无产阶级(proletariat)的混成词。 [5][6]...

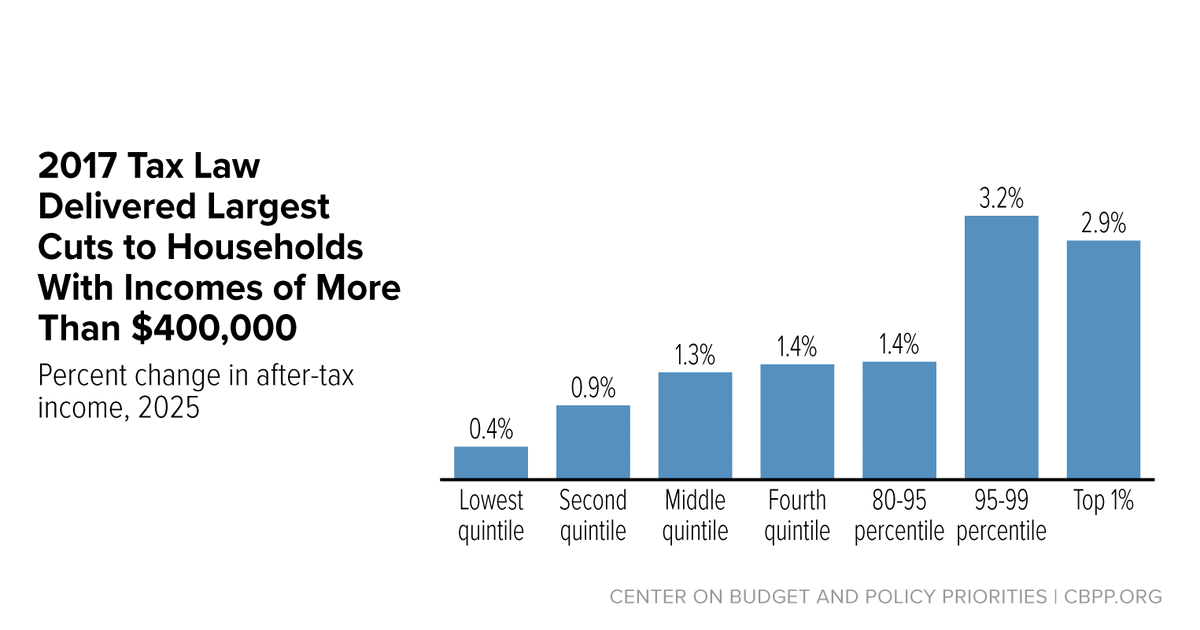

A growing body of research shows that the corporate rate cut has delivered large gains to top earners but done little for everyone else.

Policymakers and the public should understand that the 2017 Trump tax law was skewed to the rich, was expensive and eroded the U.S. revenue base, and failed to deliver promised economic benefits. A 2025 course correction is needed.

“double damage” inflicted by the wealthiest corporations and individuals who disproportionately contribute to climate breakdown through their outsized carbon emissions and who rob governments of the funding needed to address the fallout from climate breakdown by abusing tax

“Double damage” inflicted by wealthiest corporations and individuals highlights twin crises of climate breakdown and inequality The amount of tax lost every year to multinational corporations and wealthy individuals using tax havens is on par with the amount of money needed each year to cover the estimated cost of climate-induced loss and damage. In a […]

amount of tax lost every year to multinational corporations and wealthy individuals using tax havens is on par with the amount of money needed each year to cover the estimated cost of climate-induced loss and damage

The holiday season is upon us, which for the millions of dust-covered board games that have spent the year hibernating in cupboards and cabinets means making the annual pilgrimage to the family dinner table to collect the biscuit crumbs and greasy finger stains they need to sustain themselves for another a year. In honour of […]

"It’s instant replay of the same old crap. The first time they went to jail. The second time, nobody went to jail, but there were some significant financial penalties. And the third time, it was a complete pass that allowed people to get the idea that if you’re big enough and important enough, you can get away with anything. And that, I’m afraid, has permeated the society."

The latest Corruption Diaries episode is out! A new podcast episode every Wednesday: "It’s instant replay of the same old crap. The first time they went to jail. The second time, nobody went to jail,...

their wealth has grown three times faster than the rate of inflation ... The wages of nearly 800 million workers have failed to keep up with inflation and they have lost $1.5 trillion over the last two years, equivalent to nearly a month (25 days) of lost wages for each worker

The world’s five richest men have more than doubled their fortunes from $405 billion to $869 billion since 2020 —at a rate of $14 million per hour— while nearly five billion people have been made poorer, reveals a new Oxfam report on inequality and global corporate power. If current trends continue, the world will have its first trillionaire...

This inequality is no accident; the billionaire class is ensuring corporations deliver more wealth to them at the expense of everyone else…… through squeezing workers, dodging tax, privatizing the state, and spurring climate breakdown

analysis of World Benchmarking Alliance data on more than 1,600 of the largest corporations worldwide shows that 0.4 percent of them are publicly committed to paying workers a living wage and support a living wage in their value chains

But they’re also funneling power, undermining our democracies ... No corporation or individual should have this much power over our economies and our lives

Bernard Arnault is the world’s second richest man who presides over luxury goods empire LVMH ... He also owns France’s biggest media outlet, Les Échos, as well as Le Parisien

at least 228 of America’s biggest (Fortune 500) corporations — representing more than two-thirds of some 300 companies with political action committees — have given $26.3 million to election deniers during the 2021-2024 election cycles... giant corporations that announced they wouldn’t support election deniers but reversed course include FedEx, which has given the deniers $303,000 since January, 2021. Home Depot, $602,500. Johnson & Johnson, $138,000. McDonald’s, $107,000. UPS, $575,000. Verizon, $250,500. Walmart, $297,000. Wells Fargo, $244,500

They say they want to build public trust and avoid political upheaval, but they’re bankrolling election deniers

Note that these numbers show only the donations that corporations are openly disclosing — not funds they’re channeling through trade associations, super PACs, and dark money groups

And the same companies will be giving millions to the “others side” too. As my dearly departed Mother used to say, “playing both ends against the middle”

In this case, the "other side" is the United States of America

Big money has created a deep cynicism about our democracy, which Trump and election-deniers are exploiting to the hilt. Those of us who care about democracy must do more than vanquish Trumpism. We...

烏衣巷在南京秦淮河南岸,原為東吳烏衣營的駐地,故名,後為東晉時高門士族的聚居區,東晉開國元勛王導和指揮淝水之戰的謝安都住在這裏,在刘宋、南齐时期,定居于乌衣巷的琅邪王氏支系因为官位不高,门第被琅邪王氏定居于马粪巷的一支马粪诸王压倒。...